The US Government and Congress remain committed to implementing a decoupling in relation to China, which is now obvious in high technology sectors.

Since 2001, the year of China’s accession to the WTO, globalization has accelerated, with the inherent relocation of countless western companies to China, contributing with capital and technology to its development. China’s technological dependence on the US and the EU peaked c. 2009. The American commitment to decoupling in technological areas has been increasing since the middle of the last decade. The pace of China’s technological advance has scared American elites, leading US leaders to consider it a serious threat, since high technology is the engine that feeds superpowers. The first US reactions were essentially “defensive” to prevent access to relevant technologies by Chinese companies: export and import controls, limitations on investment (from and to China), restrictions on licensing in the areas of telecommunications and electronics, visa bans, rules on technology and data transfers. Lately, Washington has focused on “offensive” measures: blacklists of Chinese companies (the Communist Chinese Military Companies (CCMC) included in the Entity List, whose number reached 532 in 2022, and include companies in the technological area such as AMEC, Huawei and Hikvision), the ban on any US Person to have any relation with CCMC, financial sanctions, banning Chinese technologies for national security reasons, threats to foreign companies that continue to sell to Chinese companies (eg, AMSL) or that continue to operate in China (eg, TSMC, SK Hynix). European authorities did not go so far as the American bellicosity. But they have already approved European legislation to screen Chinese investment, and public opinion in many European countries is gradually shifting towards an unfavourable opinion on China, which has led more and more European governments to adopt measures to contain Chinese investment and companies.

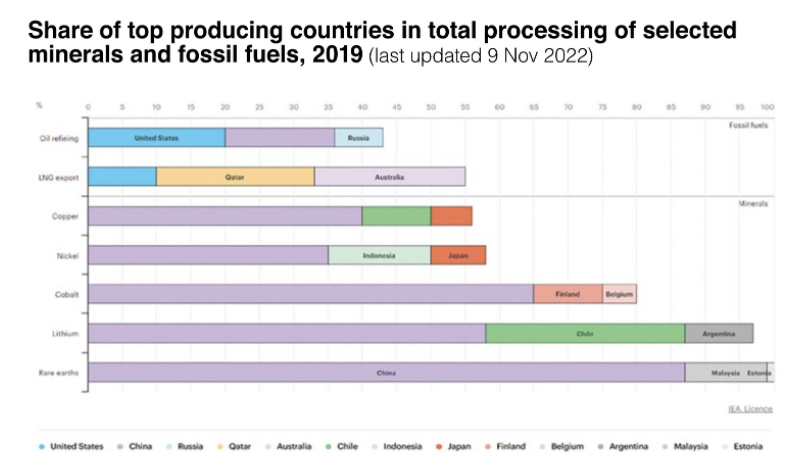

However, in spite of this historical background, in order for Europe to move forward quickly in many areas of a [greener] economy, it is important to have a non-animosity relationship with China. One of the sectors in which there is a huge [European] dependence is the production of solar panels and photovoltaic material, which will feed a significant part of the additional production of renewable energies in the coming decades. According to the IEA, Chinese companies hold at least 74% of the market share in each step of the solar panels supply chain. Other sectors crucial to accelerating the energy transition are transport and energy storage – responsible for c. 40% of the European energy mix – for whose rapid electrification it is necessary to have an understanding with China, given Europe’s current dependence on critical metals, the delay in know-how regarding gigafactories and their components and intermediate products, in addition to the huge dependence as well regarding access to the ores from which critical metals are processed from.

Europe currently manufactures less than 1% of the global total of electric batteries for EV, compared to over 90% in Asia. How did this happen? How, in some areas, did China become more advanced than Western countries?

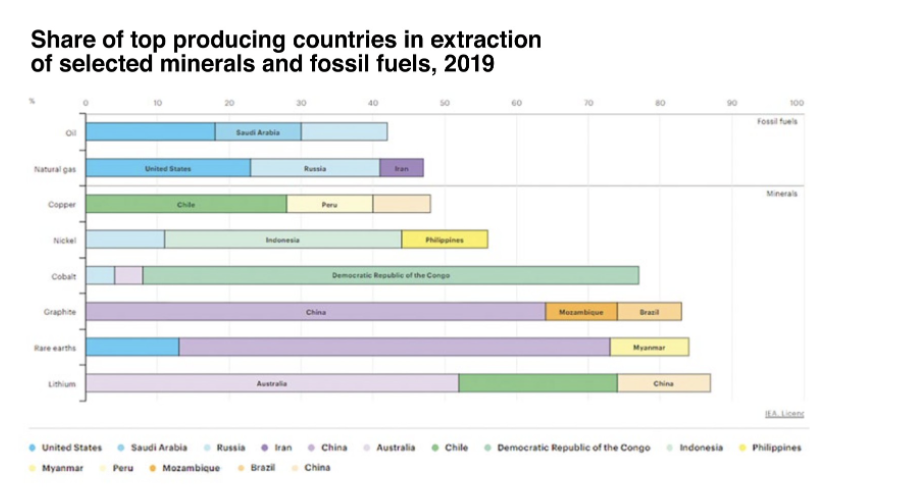

Twenty years ago, while Europe continued pushing the issue of electric mobility and storage with its belly button, in China the enormous potential of these strategic sectors was perceived to leverage a significant part of the [green] economy of the future. As a result, in execution of clear public policies (including strong governmental financial incentives) Chinese companies invested in all segments of this value chain. Massive sums were invested in R&D. Efforts were made to ensure access to ores such as lithium, nickel, cobalt, manganese, graphite, rare earth elements, copper, iron, aluminum. Some companies (Tianqi, Ganfeng) got expertise in chemically processing (refining) these ores into critical metals. Companies specializing in the manufacture of electrodes (cathodes and anodes), electrolytes and other components for electric batteries benefited from strong state support, producing these components in a complex value chain culminating in [plants integrating the value chains linked to] gigafactories. Electric vehicle (EV) manufacturers have multiplied in China – by 2021 there were >500 EV brands in the country.

The nascent European EV and gigafactories industries are dependent on supplies by Chinese companies – many of them state-owned – of electric batteries (for 5-10 years) and critical metals (in the long term, for at least 10-20 years) from China. On the other hand, given the progressive decoupling between the US and China and low customs tariffs, Europe will certainly constitute the second largest market for Chinese EVs, analysts predicting a significant growth in their market share.

By 2050, the EU estimates that its demand for lithium alone will be 16~57 times higher than today and that critical metals will soon be as important or even more important than oil and gas. It has been evident for some time now that to reach ‘Net Zero’ in 2050 (or 2060 ~ 2070, to be more realistic…) a much larger quantity of critical metals and the ores from which they come from will be needed. Public policies to achieve that goal and reduce the production of greenhouse gases imply, therefore, a significative increase in mining and refining of these ores. Those responsible for defining and executing public policies must assume this clearly.

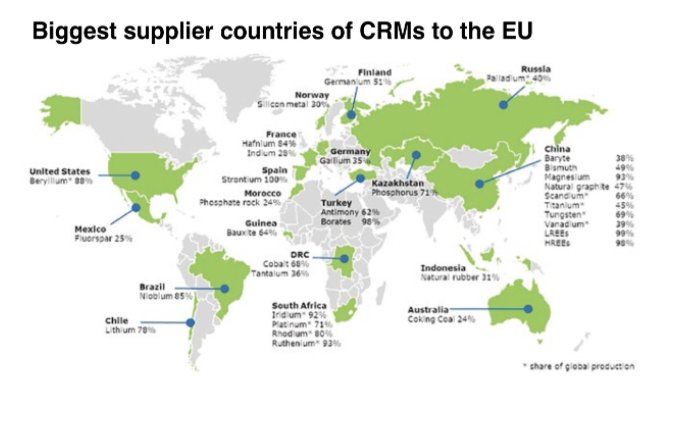

In a notable speech on the occasion of her official visit to China in March 2023, the President of the European Commission, after mentioning the Net-Zero Industry Act as a fundamental part of the EU’s Industrial Green Deal Plan, reiterated the European objective “to be able to produce at least 40% of the clean technologies we need for the green transition”. Ursula von der Leyen is aware that, in order to achieve this objective, the EU needs to be more independent and diverse with regard to the essential factors necessary for its competitiveness in the energy transition. And she openly expressed her concern about the massive reliance on critical metals “from a single supplier – China – for 98% of our rare earth supply, 93% of our magnesium and 97% of our lithium – just to name a few.”